By undertaking a planning process with a long-term perspective, there is an opportunity to develop a life insurance strategy that addresses both your pre-retirement family continuity needs and your objectives for greater security and legacy in retirement.

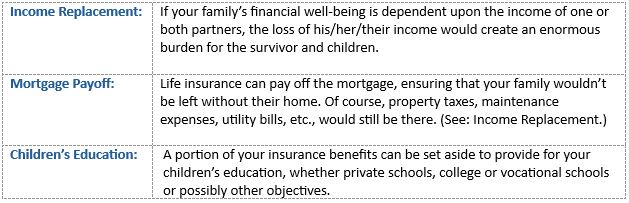

"If I Die" Insurance

Prior to retirement, life insurance is needed to protect most families from three major financial risks. This is the “If I Die” protection.

In the following graph, these needs are represented by down sloping lines as they are assumed to diminish over time.

Donovan Equipment Company, Inc. and Donovan Spring Company, Inc. (together, the “Donovan Companies”), recognized leaders in the New England truck equipment industry, have been acquired by its accomplished and long-tenured executive management team. Originally founded in Lawrence, MA, the Donovan Companies have successfully grown over several generations of family ownership to be a leading truck up-fitting and equipment dealer serving commercial, municipal and individual customers in the region.

Founded in 1932, the Donovan Companies (www.donovancompany.com) now operate as a full line truck equipment and spring and suspension specialist out of its 73,000 square foot facility in Londonderry, NH. Started by D.G. Donovan and later lead by Donald Donovan, Donovan Equipment and Donovan Spring have continued to flourish under the stewardship of Darlene Donovan and guided by its fundamental principles - quality products and great service at a competitive price.

BaldwinClarke’s investment banking division, Baldwin & Clarke Corporate Finance, LLC (BCCF) served as the exclusive buy side adviser on this transaction, assisting the executive management team of the Donovan Companies on their acquisition of Donovan Equipment Company, Inc. and Donovan Spring Company, Inc. BCCF’s advisory services were provided to help facilitate the positive ownership transition to the Donovan Companies’ experienced leadership team who have successfully operated the businesses over many years and have taken great care to maintain the Donovan tradition of excellent service to its loyal customers.

Ahh…springtime! The birds are chirping, the grass is growing, and the world is in bloom. As with most of nature, there comes a time when the young must strike out on their own. The baby birds must leave the nest, the cubs must leave the den and, most importantly, for everyone’s sanity, your children will eventually need to move out of your house. The birds and bears have it easy - unlike ducks and humans, they do not have bills. 😊

Helping a child to successfully establish independence is never easy, and more challenging now. Rent prices are through the roof. College loans, car loans, medical insurance, and the dreaded credit card bills (thanks to Uber and Amazon) can make the financial aspect of leaving home seem very scary at the least.

However, all is not lost! There are some things that you can do to help your child get ready and prepare for life outside of your house.

With the S&P 500 closing up positive on Friday 3/29/24, we can now claim a second consecutive quarter of double-digit market gains. This back-to-back performance has not occurred in 12 years. Impressive gains to say the least but that’s just a part of the story. Q1 2024 was the best first quarter experienced since 2019. And the S&P 500 has been up over 22% in the last 2 quarters (and over 27% since the bottom that we experienced in late October of last year).

2023, for the most part, was a technology-driven market. If you back out the sizable gains produced by relatively small cohort of growth stocks (the “Magnificent 7”), the overall market produced fairly mediocre returns. It wasn’t until the FED implied a change in policy intent and a pause on future interest rate hikes that the rest of the market (the other 493 companies of the S&P 500) started to claw back some ground. And that ground, so far, has been maintained.

This year we continue to witness outsized returns coming from companies that will benefit from the application of Artificial Intelligence (AI). Advancements in AI have pushed names like Microsoft, Meta, Amazon and Nvidia to new highs -- as all of these companies should continue to see business model improvements & efficiencies from this technology.

So far this year, we are seeing market participation broaden. Both energy and financials are up 12% year-to-date. The communication sector has been up roughly 15% this year and the progress being made is not all relegated to just large caps. The Russell 2000 (two thousand small companies) has recently hit it’s 52-week high.

With this backdrop, what are investors to expect going forward? Will the same market leadership continue to drive performance? And what happens if certain expectations that have been driving the markets to new levels do not occur? Expectations may need to be adjusted given where we are now.